(954) 450-1929

(954) 450-1929

Elaine Sahlins Senior Vice President HVS International — San Francisco

As evidenced in our work on a number of condominium hotel or condo-hotel projects in the past few years, the success of a condominium project is not necessarily dictated by or related to the success of the underlying hotel’s performance.

Most condominium projects are located in established destination resort markets. In the current economic environment, even with low-cost and readily available financing, development of a traditional wholly-owned full-service resort hotel is unlikely to pencil based on the increasing costs of construction.

At this point in the development cycle, it would be a rare project where the hotel would be successful without a supplementary source of cash flow from residential, fractional, or condominium hotel sales.

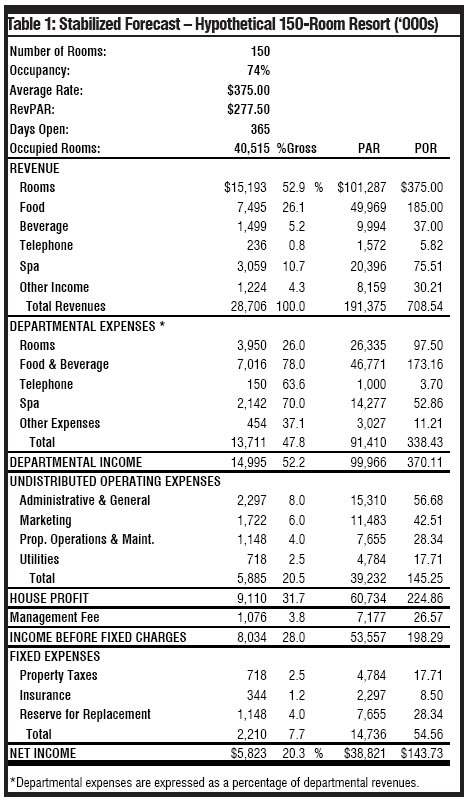

From a developer’s perspective, the same number of units designed in a condominium hotel project can more than make the project pencil, they can produce a substantial profit. To illustrate the potential profitability of a condominium hotel project, consider the stabilized operating income statement for a 1 50-room luxury resort shown in Table 1, in the box below.

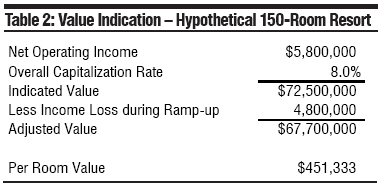

To convert the forecast into value, an 8.0% capitalization rate was used. The net present value of the loss income during ramp up was then deducted. This procedure indicates the following value.

Consider the same 50-room resort sold as condominium units. Assuming that each guestroom is roundly 600 square feet and sells for $,250 per square foot, the average sales price is $750,000 per unit. For branded condo hotel projects, a number of units are often held by the developer. The following scenario illustrates the potential value of the same property as a condominium hotel project assuming 85% of the guestroom inventory is sold:

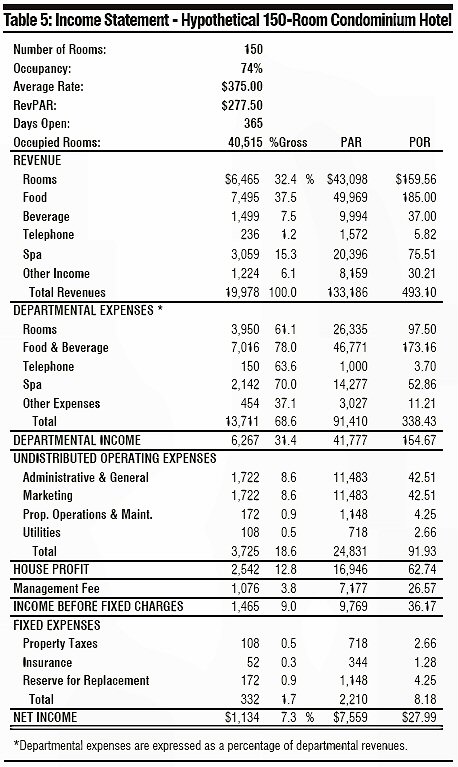

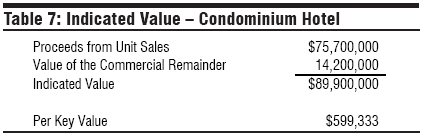

In addition to the revenue from the unit sales, the 15% of held units and the remaining commercial hotel operation yield an additional value. The income statement show earlier was adjusted for the condominium hotel ownerships for the blended rooms revenue and shared expenses. The rooms revenue calculation is set forth in the Table 4:

The developer retains all of the other revenue and is obligated to pay a share of the operating expenses. In the following example, the repairs and maintenance and energy expenses are share 85% individual owners and 15% developer while 25% of the administrative and general expenses are allocated to the individual owners. Property taxes, insurance, and reserve for replacement are allocated 85% to the individual owners and 15% to the developer. (Table 5, below)

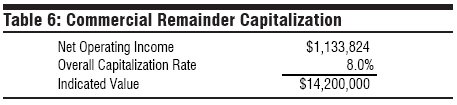

As reflected in the in the following table, capitalizing this net operating income provides roundly 19% more value to the hypothetical condominium hotel.

The aggregate value of the project as a condominium hotel far exceeds its value as an operating hotel.

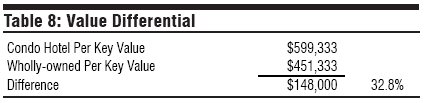

As seen in the following chart, this simplistic example shows a roundly 33% difference in the per-key value, demonstrating why successful hotel condominium projects appeal to developers.

The value difference can be considerable, particularly in the distribution of cash flows to developer. Condo-hotels generate significant cash flow either during the sales process or immediately upon completion, depending on state law.

The developer can pay down debt from the condo-hotel sales proceeds whereas the net operating income ramp-up of a new wholly-owned property would typically have debt-service shortfalls in the first year or two operations, requiring the developer to come out of pocket with additional equity.

Successful condo-hotel projects share distinctive attributes. The projects are typically located in established destinations that are easily accessible to the individual-unit owners. Successful condominium hotel projects need not be feasible as a traditionally financed hotel, but must be located in desirable destinations and designed to the potential buyers.

Joel Greene of Condo Hotel Center (www.CondoHotelCenter.com), an established broker of individual condo hotel units, maintains in his summary of 2006 trends that the most appropriate buyers of condo hotel units are wealthy individuals interested in buying a “hassle-free” vacation home. These buyers would like the rental proceeds to cover some or all of the costs of ownership and the property to appreciate, but are not typically speculators.

Condominium properties located in such destinations as Cabo San Lucas, Mexico, parts of Florida, ski resorts, and Hawaii, among others, continue to attract unit buyers and developers. Well-located and well-designed properties are expected to be successfully marketed even as the residential condominium markets soften.

The purchase of hotel condominium units by second-home buyers with disposable income is not driven by the same dynamics as those of the residential condominium or second-home buyer. Many buyers are purchasing units with the intent of using the resort for vacation as well as considering the property as an endowment for their children. These buyers have well-funded retirement plans and are not swayed by short-term residential pricing swings.

With the inherited and earned wealth currently held by older and retiring baby boomers, condominium hotel properties in attractive destination areas can be a more successful development than a traditional operating resort.

About the Author: Elaine Sahlins is Senior Vice President with HVS International’s San Francisco, California office. She holds an undergraduate degree from Barnard College, Columbia University in New York City and an MPS degree in Hotel Administration from Cornell University. After graduating from Cornell she worked for VMS Realty in Chicago analyzing hotel investments, and then went on to join Security Pacific in San Francisco, which was subsequently acquired by Bank of America.

About the Author: Elaine Sahlins is Senior Vice President with HVS International’s San Francisco, California office. She holds an undergraduate degree from Barnard College, Columbia University in New York City and an MPS degree in Hotel Administration from Cornell University. After graduating from Cornell she worked for VMS Realty in Chicago analyzing hotel investments, and then went on to join Security Pacific in San Francisco, which was subsequently acquired by Bank of America.

She joined HVS International in 1987 as a Director in the San Francisco office. Ms. Sahlins also, with Suzanne Mellen, directs HVS Gaming Services, and Shared Ownership Services in the San Francisco office.

Ms. Sahlins may be contacted at: HVS INTERNATIONAL SAN FRANCISCO 116 New Montgomery Street, Suite 620 San Francisco, CA 94105 (415) 268-0347 tel. (415) 896-0516 fax esahlins@hvsinternational.com