(954) 450-1929

(954) 450-1929

Beginning of a Real Estate Boom, Not an End

By Bob Waun

Outline

The Case for Explosive Condo Hotel Sales Potential

I. Why the Bubble Statistics fall short:

a. The Bubble Debunked

b. The Refinance/Renovation Effect

c. The Redevelopment Effect

d. The Currency Effect: Why Foreign Buyers Matter

e. Why Interest Rates Matter

II. The Population Data:

a. Why Boomers Matter

III. The Wealth of Nations Effect: Earned and Inherited

IV. Finite Supply: Sun, Shore, Slopes – the world wants the same things

V. Why Condo Hotel: Ownership Option Increases Affordability and Lifestyle

VI. Conclusions

This paper intends to make a case for three key points: 1. Real estate statistics showing national appreciation figures are miscalculated and misleading, causing alarming reaction to reasonable market appreciation in most cases.

2. The Baby Boom population is going to demand second homes, and is bigger than just U.S. boomers.

3. The market for condo hotel units and innovative forms of second/retirement home ownership is on the verge of a boom, not a bust.

I. The Bubble: Debunked

Our media has dramatized the entire U.S. real estate market as ‘overheated’, ‘bubble like’ and ready to crash at any moment. Even conservative economists point out that there are only pockets of ‘froth’.

Real estate is NOT red hot all across America. In fact, many mature U.S. real estate markets are soft, measured in real (inflation adjusted) terms they may even be declining in value.

But media has a hard time making a 0.3% home appreciation rate in the industrial Midwest news, while 28% gains in once rural or underdeveloped areas of Arizona or Florida are exciting headline news.

Midwestern populations are migrating to sunny, Southern and Western States at increasing rates, by purchasing “future residences.” The trend is evident, but quiet, because many northerners are maintaining 2 residences for the time being. But will there be a mass exodus when the bulk of boomers retire?

Is the real story not the over heated markets of the south and resort/second home areas but rather the future potential implosion of values in the heart land? Is the bubble actually in the markets with low appreciation rates?

What is an appreciation rate, and who is measuring these stats? The National Association of Realtors, The Federal Home Loan Bank, Fannie Mae, and The Federal Reserve all have a role in compiling the statistics. But what is disturbing is the lack of economic reason that seems to enter the public debate after the official statistics are released to the media.

The media announces that a home in the Southeast rose by 14% in value, Northeast by 9%, Midwest by 4% and in the West by 13%. This would lead a $100,000 home owner in Utah to believe he gained $13,000 while the San Fransican gained the same amount?

There is no discussion of inflation adjustments, or renovation investments, or regional job or emigrant growth, all factors that might have effected the real gain. How does such a useless statistic as ‘appreciation rate’ even find it’s way to page 12, let alone the headlines? Markets are regional, and regions are micro, not macro-economic studies. Consider appreciation then in an individual micro-economic example.

The Refinance/Renovation Effect

In 1998-2003, low interest rates ignited record home refinancing, many homeowners pulled “cash out” to reinvest in their homes:

A $100,000 home in 2000, with $60,000 in debt may have been refinanced to $75,000 (75%), with $15,000 cash out going right back into the home in capital improvements.

This home then sold for $120,000 in 2001, wealth was created, but less than the statistics assume. Did it rise by 20% in “appreciative” value? Or did the improvements and borrowing just increase the value?

National statistics measure this as a 20% rise. You decide, then multiply by your neighbors who added additions to their 1940’s bungalows between 1999-2005. If the national appreciation rate was recalculated to account for home renovation expenses, real gain in value would be determined and would be a much more calming and useful statistic to determine if housing is ‘overheated’.

The Redevelopment Effect

America’s housing stock in 2000 was on average 47 years old. The rise in Home Depot stock should be a market indicator of where Americans are shopping – home improvement. At the same time urban areas are seeing unprecedented regentrification. When a blighted area is improved, values go from zero. The calculated appreciation rate is spectacular.

Farmland to Suburbia

Don’t the Housing Statistics adjust for this effect? NO. For example, when a corn field sells for $5000 an acre, then $50,000 per lot, then $500,000 per home the stats reflect an appreciation rate without regard for the capital investment that went into this meteoric rise.

The Currency Effect: Inflation/Deflation, Quiet and Invisible at First

The frothiest real estate markets are also the most popular with foreign buyers. Is this a correlative or causal effect? The U.S. Dollar has fallen against the EURO by 11% since July 2003.

For real estate buyers spending EURO, an 11% rise in second home prices is invisible. With official inflation at 2.8%, a 14% rise in prices is static to European Investors. Incomes in Europe have also outpaced U.S. wages by another 4.1%. Therefore, U.S. property values could rise 18% higher with no additional cost a European buyer.

This fact is very important to real estate appreciation rates. Foreign buyers can purchase relatively easily, but cannot sell any faster than U.S. owners and will can sell at lower relative values if the currency trend switches. Markets where high concentrations of foreign buyers exist will be more volatile for this reason.

For South American buyers, our real estate has been a good hedge against inflation in their countries. In Japan, where rates of return are nearly negative, the incentive to invest in the U.S. is also encouraging.

The Interest Rate Effect: Reversion to The Mean?

Will appreciation rates revert to the 30 year mean of 5% (or below) when interest rates rise? Real estate values have risen due to the low ‘cost of capital’ since 1998. Certainly low rates have added fuel to the speculative fires of real estate investors, and froth has been created by easy money.

Zero down loans to first-time home buyers, easy no-doc loans to investors, banks competing for borrowers, even the Internet have all made capital less costly and driven the real estate market higher.

Fannie Mae scandals are tightening lending requirements. Concern over all the ‘bubble press’ itself have made lenders edgy. Will there be a shock to bond/rate markets if foreign investment tapers off? What effect will these and other unforeseen events have on the easy mortgage environment that will make some ‘deals’ less closable?

While U.S. banks are considering trimming real estate exposures, by decreasing their holdings of residential mortgages by 9% since 2003, Non-U.S. banks have filled this void.

As U.S. consumers save less, savers in the developing world have purchased our securities at a record pace. As unsecured credit card balances have been transferred to home equity lines, Baby Boomers have begun to inherit “The Greatest Generation’s” enormous cash savings stockpile. Will the Transfer of Wealth change everything?

The Transfer of Wealth: 20 More Years

Demographic analysis disputes the facts of whether this transfer began in mass in 1997, 1998 or 1999, but one fact is clear, it is a 20+ year wave that won’t end until $17 trillion of wealth is transferred within our population by 2018-2020.

With or without Social Security, these funds will be required to keep the Baby Boom generation at the standard of living to which they have become accustomed. What will retirement look like for Baby Boomers? Many believe it will look like whatever Boomers (or Zoomers) want it to, even if they have to borrow to get the lifestyle.

Leopards and Spots

Boomers are not about to change their lifestyle dramatically in retirement. New ways to afford an exciting retirement will be invented by this dynamic generation. The real estate boom will continue because boomers demand home ownership, real estate has worked in their past, and they will find ways to make it work for their lifestyle demands of the future.

Boomers will demand more of less, the most coveted places and spaces will be driven to stellar levels, because this is a generation raised on competition for the best against a large cohort of competing players.

II. Population Data

A Large Cohort: Boomers Around The World

A Large Cohort: Boomers Around The World

A Large Cohort: Boomers Around The World

A Large Cohort: Boomers Around The WorldAmerican Boomers often think of The Rolling Stones as an American band of their generation. So do the Brits, French and Germans… and Japanese. The media has touted the 78 million U.S.

Baby Boomers who will retire in the next 15 years (the largest population turned 50 last year, with 50th birthdays occurring every 7 seconds), but there will be 103 million Empty Nesters in Europe by 2009. Japan will have 32 million boomers by 2010, in a total population of only 127 million people. 213 million Boomers competing for a uniquely similar lifestyle in retirement.

213 million Baby Boomers, all raised on Hollywood, Disney and The Stones? All experiencing the same trans-generational inheritance from the ‘greatest saver generation’. Even in Japan where savings is a national virtue, the baby boomer generation grossly out spends the previous (WWII) generation. The baby boom generation was the first cohort of the 20th century to embrace debt, spending over thrift, and a global economy.

How many of these 135 million World Boomers will opt for a retirement residence somewhere on U.S. soil? If just 10% of the European & Japanese boomers choose the USA, our population could increase by 13 million or nearly 900,000 higher net worth boomer retirees per year. Whole new cities could be, and are being formed.

This statistic leaves out so many other world Boomers with the means to choose the U.S. Lifestyle in retirement. But starting with 213 million Boomers proves the point, demographically something big is happening.

In an age when our media pines over our trade deficit, we need to recognize our unique export in which we truly have a competitive advantage – our lifestyle. First world health care, economy, security, free and open borders, entertainment, a relatively low taxation rate, stable currency and markets, and lastly – a historically appreciating real estate market.

So is there a bust after the Baby Boom retires in America? First, demographic data suggests that incomes of the previous generation did taper off between age 45-54, but researchers believe Boomers will delay their exit from the labor force – and forestall any decline in household income – in the same way they delayed marriage and having children.

As a result, Boomers may enter their mid-50s and 60s with their household income undiminished – a change in a demographic pattern that would create huge investment and business opportunities.

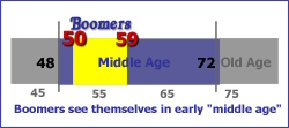

With age 65 still 15 years away for most boomers, this spells a wave of consumption that should continue. Boomers over 50 think of themselves in early “middle age” and that “old age” is still almost 20 years in the future.

It should be a national priority to court the world’s wealthiest soon-to-be retirees. Many of the fastest appreciating real estate markets in America are already experiencing the benefits of these new emigrants. No longer in huddled masses, they arrive on first class and private flights or in yachts.

As the oldest baby boomers become senior citizens in 2011, the population 65 and older is projected to grow faster than the total population in every state. In fact, 26 states are projected to double their 65- and-older population between 2000 and 2030.

Florida, California and Nevada would each gain more than 12 million people between 2000 and 2030. Arizona is projected to add 5.6 million people, and North Carolina, 4.2 million, Texas and Utah each would add 3 million new residents.

As a result, Arizona and North Carolina would move into the top 10 in total population by 2030 – Arizona rising from 20th place in 2000 to 10th place in 2030 and North Carolina from 11th place to seventh place. Michigan and New Jersey are projected to drop out of the top 10.

The projections indicate that the top five fastest-growing states between 2000 and 2030 would be Nevada (114 percent), Arizona (109 percent), Florida (80 percent), Texas (60 percent) and Utah (56 percent).

Most (88 percent) of the nation’s population growth between 2000 and 2030 would occur in the South and West, which would be home to the 10 fastest-growing states over the period.

The share of the population living in the South and West would increase from 58 percent in 2000 to 65 percent in 2030, while the share in the Northeast and Midwest would decline from 42 percent to 35 percent. The Big Chill, when boomers shift preferences, is as real as the boom itself. The Echo Boom generation, or the Boomers’ kids, will not sufficiently feed demand for 7-9 years. This effect on real estate values is beginning to show up in single family suburbia through out the industrial and middle western states. While the echo boom generation is also seeking starter condos and lofts, the Bust generation is demanding the larger yards for their 30’s child-rearing years. Is it any wonder that condo sales are stronger than any time in U.S. history?

III. The Wealth of Nations: Earned and Inherited, Where is the Money Coming From?

The World’s population is growing at the fastest rate in Developing Countries, not in the Developed World.

Most of the World’s population cannot consider a second home in the United States.

In 1998-2003, low interest rates ignited record home refinancing, many homeowners pulled “cash out” to reinvest in their homes: even the first world, but the people who can, will choose the U.S.A.

In just Europe and Japan, there are 213 million boomers entering the “empty nesting” phase of life. Mobility has never been easier why not work from The States for a couple months in the winter?

Certainly, America has many desirable lifestyle features. But there is something more at work than weather, and democracy. Currency fluctuations of the last 2 years in favor of European and Japanese have made buying a piece of America advantageous.

If a foreign buyer signs a purchase agreement for U.S. $200,000 and the Euro rises 5% against the Dollar before closing, he effectively purchase the second home for U.S. $190,000. If in the same time frame the property value has gone up 5%, to $210,000, he has, in his mind gained U.S. $20,000 or a 10% return.

Now that he is invested in The U.S., he will hope for the Dollar to rise again before he sells and repatriates his Dollar profits to Euros. And if foreign buyers continue to purchase our real estate, the Dollar may just bounce back sooner rather than later.

Since the rest of the world has experienced similar low stock market returns and low interest rates, a double digit return in blue-chip U.S. real estate that has the added benefit of a sunny holiday, looks good around the globe. Boomers globally are inheriting the WWII generation’s wealth.

So the image of the wealthy foreign visitor is growing, and somewhat real, but certainly there is an 80/20 rule at work. Not every foreigner is becoming a conspicuous consumer of U.S. real estate because of the Dollar’s decline? In the U.S., 73.5% of U.S. boomer households have under $150,000 in wealth. As many as 47% of boomer respondents surveyed in the 2002 Cost of Leisure Index by Allstate Financial say that they will continue to work after retirement. So how big is the second home market? Can even the majority of boomers (U.S. and abroad) afford 2 homes?

The 80/20 Rule has become the 73.5/26.5 Rule

Over the next 15 years, it is estimated that Boomers will get the biggest slice of the inheritance pie: $17.8 trillion. Distributed evenly, each of the 78 million U.S. boomers get $228,205. But these inheritance dollars will not be distributed evenly.

The 73.5% of the boomer cohort without wealth, will likely join the wealthier classes. Let’s assume the distribution is close to 73.5/26.5? Within the next 15 years, 20.7 million boomers will become over $658,000 wealthier, and 57.3 million people will get $72,900 to boost their meager net worth/retirement.

Is the market for a luxury second home reduced to only the top 26.5% or 20.7 million people? Or will the 57 million 50 year olds with a $150,000 net worth be able to save enough to live the dream?

Boomers: Conspicuous Spenders or Savers and Investors?

Americans used to save and invest their bequests. No more. The sputtering stock market has prompted Americans to consider other options if they receive a $25,000+ inheritance. Boomers are more likely to spend the money than other groups.

Ever the optimists, Boomers believe that many more of them will get inheritances, and for larger amounts than previous research has suggested, according to a survey of 1,204 Americans conducted by Knowledge Networks for American Demographics. And contrary to their image as conspicuous consumers, Boomers claim they plan to put the money into savings, pay down debt or invest in a retirement home.

IV. Finite Supply: We All Want the Same Thing

This is such a debateable fact, I want to make my point swiftly: “I’ve lived richly, and I’ve lived poorly… rich is better.” If the boomers can afford to live richly, they will.

What Housing Do Boomers Plan to Spend Their Money On?

According to a Harvard study, “baby boomers, are expected to make up 20 percent of the population by the year 2030. Baby boomers already comprise the single largest group of homeowners – nearly one-quarter of all homeowners – with 75 percent of those over the age of 50 owning their own home. Research shows that boomers are looking to second home ownership as a smart investment opportunity.

Considering that boomers are starting to think differently about real estate investments as part of their retirement plans, the U.S. Census Bureau predicts second home purchases for boomers to reach 6.4 million units by 2010, up from 5.5 million units purchased in the 1990’s.

According to NAR, investment homes accounted for a quarter of all home purchases in 2004, and vacation home purchases an additional 13 percent.” According to a Coldwell Banker survey “Affluent Baby Boomers Are Not Ready to Stay in Their Current Homes Forever.” Today’s Boomers are not slowing down, and the majority remains “on the move. They want luxurious homes and want to remain active. They are in their peak earning years, have benefited from many years of strong stock market returns and have built tremendous equity and appreciation in their homes. These factors, along with many receiving inheritances from their parents, are allowing the luxury home market to thrive and it should be robust for years to come.”

V. Boomers will choose New Options for Second Home Ownership: Condo Hotel

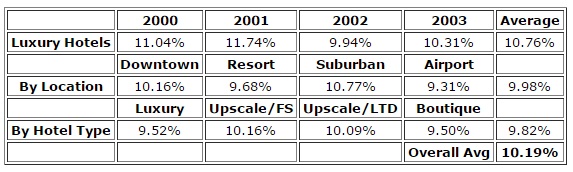

Active and dynamic retirement lifestyles require either a substantial net worth, or creative new ideas. Luckily the boomer generation is adapt at innovation and leverage. The concept of Condo Hotel is not a new invention, but the Condo Hotel-Resort is a new evolution. More than just a hotel room/suite, condo hotel units sell at a higher price-per-square foot multiple (10-25% premium, $300-1000 per square foot) to a traditional condo, and are typically smaller. Successful projects will have location, quality, amenities and services that are superior. Boomers will buy for the central location, spa/health club services, and of course maid/valet/concierge services round out the dream lifestyle. Condo hotel units often do not have kitchens or have efficiency kitchens. But for a generation that perfected dining out, and the trophy kitchen – been there, done that — what are they serving downstairs for dinner? How many boomers want to retire to a hotel room for a few months every year? This is a generation that has spent 5 days a week building up frequent flyer mileage perks, a 2 days at home. After a year or so back at the ranch, where will they feel most at home? And what about all your stuff? Most boomers will not choose to live in condo hotel units for more than a couple months a year, the last generation settled for a mobile home in the sunshine for the winters, but this generation is accustomed to desiring a little more. They will want more than one residence, and if they can figure out how to afford several homes, the sky is the limit. How does a boomer buy a hotel room? Can this luxury be afford to the 76.5% of less wealthy boomers? The answer is yes, condo hotel is just one of the new evolving second home ownership options that offer a more affordable choice than a traditional second home. Between 2000-2003 the average price of a “luxury” hotel room was $239,066 ($415/sq ft), down 18%, because hotels are bought and sold based on a capitalization rate (Value/NOI = Cap Rate). As income rises and falls, hotel room values fluctuate.

U.S. Hotel Costs 2000-03

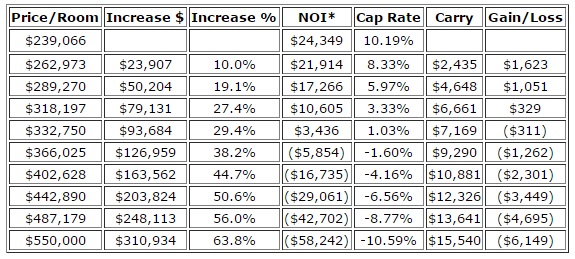

But residential condo values are not determined by income, but rather demand for ownership. In the “boomer-desirable” markets (especially those with foreign buyers) condos climbed to prices that nearly matched the price-per-square foot of full service luxury hotel rooms ($350-600/sq ft). Hotels capitalization rates are hard to gain accurate data on, and hotels are underwritten more as a service business than real estate by most lenders, so separating the real estate ownership component from the business operations is similar to a corporation doing a sale-leaseback of facilities, it can benefit all parties. Between 2000-2003, an estimate of cap rates demanded by hotel buyers was 10.19%, for the condo hotel suitable markets nationwide.

U.S. Cap Rates

If condo hotel buyers are seeking personal use, services and amenities, then accepting a lower cap rate, or none at all, might still be a reasonable and desirable investment. With the added value of tax deductions of a rental property and possible real estate appreciation, and a condo hotel buyer may even be able to justify spending money every month or having a negative cap rate of 10%.

Condo Hotel Buyers Accept Lower Cap Rates… But for How Low? (Before Split)

*NOI = Net Operation Income At a 1.03% cap rate, the condo hotel/room is worth $332,750, a $93,000 increase in value to $578/sq ft, still in the range of some traditional condo prices. If the condo buyer pays more, he simply has a subsidized second home, that is professionally rented and maintained for a hassle free vacation/retirement ownership opportunity. The consumer of this condo hotel unit also has the potential to offset their entire second home expense.

Potential vs. Real Income

A couple of big holes can be poked in this ideal picture. If the condo hotel unit owner decides to use his suite for the entire high season, he can erode much of its income potential. Since the condo hotel unit owner often shares in the expense of the professional maintenance/management of the unit, dues expenses can be higher and vary more than a traditional condo. Lastly, since future buyers will likely be drawn to owning a condo hotel for many of the same desires to ‘offset expense’ or better afford this second residence, the value of the unit may be tempered by the income it produces, or doesn’t.

Macro-Economic Forces: Condo Hotel Values

If interest rates rise 1%, assume 6.5% to 7.5%, and real estate is strictly valued for the income/cap rate it produces, the value of this $332,750 condo hotel unit may fall by $14,755 (4.4%). Higher rates, should in theory, also strengthen the U.S. Dollar, which could also have an added negative effect on real estate values. Stronger dollars could also reduce tourist demand for rooms, and lower NOI. On the positive side of the ledger is sheer boomer demand. Over the next 15 years, 291 boomers will reach retirement age and demand new residence options to fit an active, luxurious lifestyle.

If only 1% of this generation demands condo hotel as a second home option, 1.45 million units will be needed. That’s 96,600 condos per year, every year. If we assume there are 12 key markets in the U.S. for condo hotel resorts, then there will be 8,050 units per year in each market. Demand will grossly outstrip supply.

IV. Conclusions

Harvard, NAR, and NAHB all agree Boomers want to buy luxurious second homes, and will likely spend their inheritance and present residential home equity to downsize to multiple residences with similar features, amenities and locations. Demographics, and life cycle, can predict future demand. Boomers will afford this real estate the same way they bought all their previous homes, with debt leverage. U.S. Boomers will compete with foreign boomers for the same desirable retirement and second home real estate. Prices of the best properties have already soared, and will continue for at least 10-15 more years as the Boomer generation approaches retirement. “The Current Bubble Theory” has one gapping hole, When: 2005 or 2020? The answer is when domestic interest rates rise above 9%, and the dollar simultaneously begins to strengthen against world currencies and boomers (around the world) decide they have found the perfect piece of retirement paradise. The Bubble will inflate, at varying rates, until all three things occur. Most boomers desire luxury and amenities found in resorts when planning their active retirements. Less than 20 million (26.5%) U.S. boomers will be wealthy enough to afford a whole-ownership second home without rental income. Condo hotel offers subsidized luxury that will be a growing choice of savvy boomers. America should be marketing our rich lifestyle to the world’s boomers, borders are disappearing, why not live in the greatest nation on earth? Boomers will get creative by purchasing a combination of a primary residence, Condo Hotel and Fractional and PRC ownership options, to more efficiently use their limited nest eggs and to have active and dynamic golden years. If only 1% of boomers demand condo hotel, 1.45 million condo hotel units will be demanded by Boomers over the next 15 years. Demand will outstrip supply.

Bob Waun has 18 years of experience in mortgage banking and is CEO of Michigan- based Vacation Finance.